COVID-19 has triggered an economic shock like no other in living memory. Social distancing and trading restrictions hit small businesses particularly hard, with many seeing revenues evaporate overnight: nearly half of small firms reported a reduction in sales of over 40% at the height of the first wave in May 2020, according to one survey.

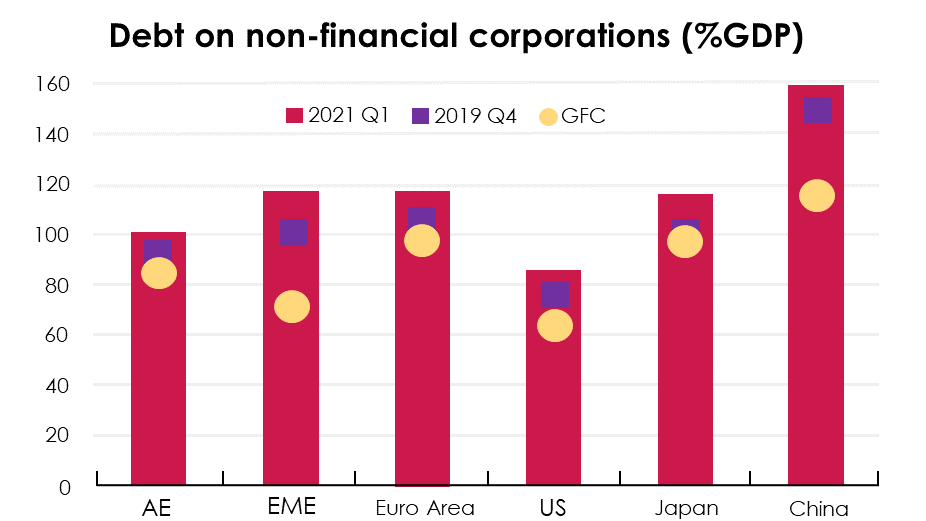

Government support has helped many businesses survive, with bankruptcies remaining below pre-crisis rates. Yet such support has come at a cost. In 48 out of 55 countries covered by a recent OECD study, support came at least partly in the form of repayable loans. The chart below shows the rise of debt of non-financial corporations and the massive growth of government guaranteed lending during the pandemic, well above the levels attained during the Global Financial Crisis.

Increase in indebtedness and guaranteed loans

Sources: OECD, forthcoming. “Financing SMEs and Entrepreneurs 2022: An OECD Scoreboard”

Note: Panel A : authors calculation on BIS data. Panel B shows the year-over-year median growth rate of government guaranteed loans across OECD countries, as a percentage.

Although there are significant differences between countries and sectors, the combination of the continued impact of the pandemic and support through debt finance may leave many SMEs with a heavy debt burden. It is therefore essential to minimise the risk that a potentially further escalating debt burden weighs down the recovery.

The growing weight of debt

Governments are now beginning to get a sense of the scale of the challenge. In 2020, the outstanding stock of SME lending grew in two thirds of countries for which we have data. The Bank of France estimated that by December 2020, French SME debt reached EUR 523.7 billion, reflecting a 20% rise in the uptake of credit during 2020. In the United Kingdom, where SME indebtedness rose by around 25%, 5.5% of SMEs were already in arrears on their outstanding loans or formally defaulting by 2021 Q1, compared to 3.6% in 2020 Q1.

These developments risk triggering a significant wave in SME bankruptcies, also because many costs have only been deferred. This includes debt and interest payments on emergency loans extended during the pandemic, whose grace periods are also coming to an end. Although a rise in bankruptcy rates may in part reflect a return to pre-pandemic levels, SME debt developments should be carefully monitored.

Recent OECD modelling suggests that a non-negligible portion of firms may become distressed and face difficulties to cover their interest expenses, threatening the recovery. Moreover, even firms that can cope with the additional debt burden are likely to scale down investment over the longer term as they seek to improve their balance sheet. For instance, our report indicates that a 7 percentage points increase in firms leverage could on average reduce investment ratios by approximately 2 percentage points. And both financial distress and reduced investment could trigger broader economic impact through income effects, supply chains, and lender behaviour, with the risk of setting back prospects for an inclusive recovery fuelled by investment in green, digital solutions.

Addressing the debt burden: the double meaning of lightening

We need to find ways to reduce the load for SMEs that would otherwise be viable, but for the temporary impacts of the pandemic. First, this requires stepping up the monitoring of SME debt developments to ensure that policy makers have sufficiently granular information to take into account the different situations across sectors and firms. Second, it is essential to better target support measures to viable SMEs that really need them, also to limit the risk of hampering the exit of non-productive firms from the market. Third, a wider range of policies needs to be considered to help alleviate the impact of debt on viable SMEs. The OECD has highlighted some key measures that can help, including:

- Repaying loans through taxes: There is increasing debate about the possibility of linking emergency loan repayments to businesses’ returns through taxes.

- Converting loans to grants: This would most directly deal with the burden of debt for firms, but, at the same time, it would transfer the burden to governments who may have limited fiscal space.

- Converting loans to equity: This process would allow emergency loans to be converted to equity if a borrower is unable to repay. This type of instrument could be attractive for SMEs as well as for lending banks, but estimating the market value of debt agreeing an exchange ratio is far from straightforward.

- Initiatives to restructure SME debt: Pre-insolvency procedures are associated with a higher rate of success, as they speed-up resolution and should be implemented when possible. The simplification of administrative procedures can also help SME restructuring.

- Ensuring an efficient liquidation process and providing the institutional conditions for entrepreneurs to exit and make a fresh start to respond to potential structural reallocation needs.

Together these measures can help lighten the load on the corporate sector and secure a stronger recovery. However, the pandemic exacerbated structural issues and vulnerabilities that left SMEs highly exposed. Hence, in addition to addressing the debt burden and legacy of the pandemic, recovery packages will also need to look forward and support SMEs to become more productive and more resilient to the challenges ahead. This includes enabling SMEs to catch up to larger firms in the use of digital tools and strengthen their management skills, as well as stepping up actions to help SMEs embark on the green transition. It is essential that support measures for recovery also reach SMEs, to effectively lighten the load and enable them to invest, grow and build their resilience.

Lilas Demmou is a Deputy Head of Division and the Head of the Financial Policy, Investment and Growth workstream at the OECD Economics Department. She has been at the OECD since 2010 and she is currently working mainly on the link between finance and productivity. Before joining the OECD, Lilas was economist at the French Ministry of Economy for three years and a post-doctoral scholar at the Paris school of Economics, Erasmus University and London School of Economy. She holds a Ph.D from the University Paris VIII. Her main area of interest are innovation and productivity, international trade, and labour market.

Guido Franco is currently an Economist at the Economics Department of the OECD, where he has been working since 2018. He obtained a Ph.D. in Economics from the "University of Rome Tor Vergata". During his doctoral studies, he participated to the Graduate Program at the Einaudi Institute for Economics and Finance and worked as an external consultant for the Inter-American Development Bank. His main research interests are in productivity, misallocation, firm dynamics and, more generally, applied economics.

Stephan Raes is a Policy Analyst and Advisor at the OECD Centre for SMEs, Entrepreneurship, Regions and Cities, where he works on the OECD SME and Entrepreneurship Strategy and the monitoring and analysis of SME and entrepreneurship policy responses across OECD countries to the COVID-19 pandemic. He previously worked as Director for Strategy, Research and International Affairs at the Netherlands’ Ministry of Economic Affairs, Minister Economic at the Royal Netherlands’ Embassy in Washington DC, and Head of the Economic Affairs team at the Netherlands Permanent Representation to the EU in Brussels. He has a Master’s degree in European Studies and a Ph.D. in Immigrant Entrepreneurship in the context of changing Global Value Chains (University of Amsterdam).